The United States is one of the only developed nations without a national industry competitiveness strategy. Some of this failure stems from a hyper-partisan political environment; but the main culprit is groupthink. Few policymakers, pundits or economists understand U.S. competitiveness problems in ways that lead them to support such a strategy. Too many policymakers, pundits, and purported experts deny there is a problem. And most view the problem and solutions in a way that precludes needed action from being taken.

To be sure, this “deficit of the mind” has gotten decidedly better in the last few years as it has become clearer to many on both sides of the aisle that the federal government needs to act, if only to counter the technology challenge from of China. But altering U.S. economic policy is like turning an ocean tanker. In this case the first step reprogramming the intellectual logic chain that has held Washington on the same, faulty course for so long.

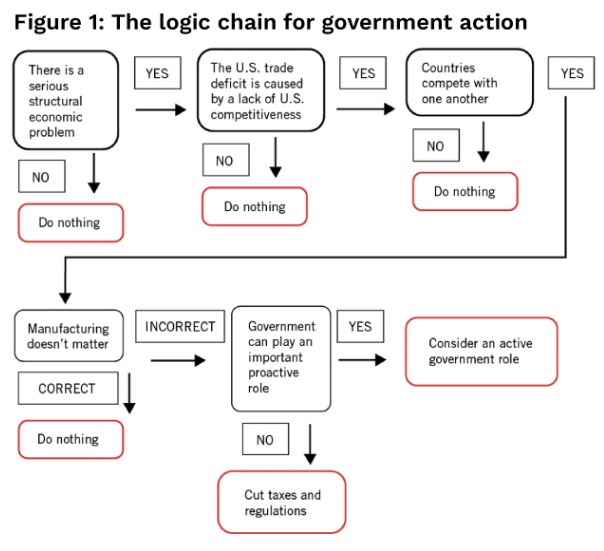

Changing policies requires changing minds. What follows are the nine most important flawed concepts that must be dispelled.

Five Reasons Policymakers Fail To Recognize They Should Do Anything To Address Competitiveness

Before policymakers can act, there needs to be a consensus that there is a problem, and a role for policy in solving it. When it comes to competitiveness, too many in Washington don’t recognize this.

Flawed Concept #1:

There Is No Problem

The first step toward restoring America’s advanced-industry competitiveness is to admit that the United States has lost ground. Unfortunately, the consensus view among many policy elites is that America is still number one.

There are two main strains of triumphalist sentiment. The first comes from the U.S. foreign policy establishment, which cannot envision decline under its watch. In its view, while there may be occasional bumps in the road – such as the Trump presidency – nothing can keep the United States from fulfilling its pre-ordained destiny. Harvard’s Joseph Nye, with his claim that “America may not actually be declining, but those predicting it are ascending,” is the patron of this group.1 Larry Summers reinforced this view when he wrote, “In many ways, U.S. concerns over China and technology parallel concerns over the Soviet Union in the post-Sputnik missile gap… or over Japan in the late 1980s and early 1990s.”2

The second group is bankers and investors who view the U.S. economy through a financial lens and see nothing but success. They ignore production in favor of financial metrics, especially the strength of the dollar and the stock market. In his Foreign Affairs, article “Comeback Nation: U.S. Economic Supremacy Has Repeatedly Proved Declinists Wrong” Ruchir Sharma, argued during the 2010s, the United States not only staged a comeback as an economic superpower but reached new heights as a financial empire, driven by its relatively young population, its open door to immigration, and investment pouring into Silicon Valley … the 2010s turned out to be a golden decade.

A golden decade if you are a shareholder or Wall Street trader—since stock market values boomed—but not a golden decade for the trade deficit, productivity growth, or wage growth.

If America is booming and past concerns about competitiveness were nonsense, why do anything?

Flawed Concept #2:

The Massive U.S. Trade Deficit Is Our Fault (i.e., We Don’t Save Enough)

One key indicator of America’s competitiveness challenge is its chronic trade deficit; close to $1 trillion dollars in 2021. If the U.S. was more competitive, it would export more and import less. But the defenders of the status quote taken off the table one of the most important indicators of declining competitiveness: the trade deficit. Conventional economists say that low U.S. savings requires overseas borrowing, which by definition requires running a trade deficit. Even the Council on Competitiveness claims that the trade deficit “stem[s] from global financial imbalances rather than from the inability of American companies or American workers to compete in global marketplaces.”3 But as economist Robert Blecker stated, “This identity does not prove causality, and is consistent with other causal stories about the trade deficit.”4 In other words, low savings are a function of the trade deficit.

Flawed Concept #3:

The United States Is Not in Competition With Other Nations

By definition, countries put in place competitiveness policies to compete with other nations. But if you don’t believe economies compete, a competitiveness policy would have as much use as an inflatable dartboard. Remarkably, a large share of U.S. elites refuse to believe that the United States competes with other nations. Paul Krugman reflected this consensus when he wrote, “The notion that nations compete is incorrect … countries are not to any important degree in competition with each other.”5 But the reality is that as the United States has lost high-value-added sectors due to falling competitiveness, sectors with lower value added have taken their place, lowering wage and productivity growth.

Flawed Concept #4:

Potato Chips, Computer Chips: What’s the Difference?

Perhaps no canard has been more damaging to the prospects for putting in place a national innovation and competitiveness strategy than the belief that America should be indifferent to what industries comprise the economy. Reflecting this view, President George H.W. Bush’s economic advisor Michael Boskin memorably quipped, “Potato chips, computer chips, what’s the difference? A hundred dollars of one or a hundred dollars of the other is still a hundred dollars.” But there is a difference, and it is profound. Hollowing out advanced manufacturing sectors, like computer chips, means U.S. adversaries such as China will be able to gain a sustainable advantage over the United States, both economically and militarily. This is why both chambers of Congress have passed the CHIPS Act legislation to support the semiconductor industry.

Flawed Concept #5:

Unshackled Entrepreneurs Are Enough

It’s one thing to acknowledge the problem and admit the United States is in stiff competition; it’s quite another to argue that the United States needs a proactive strategy. And many who are willing to acknowledge a problem think the solution is for government to largely get out of the way. In the Wall Street Journal, Former Republican Senator Phil Gramm and American Enterprise Institute scholar acknowledge the economic challenge from China, but argue that America’s success “has come from the relative absence of government planning and subsidies.”6

In fact, historically the federal government’s strategic support for new technologies has been a critical feature that has enabled entrepreneurs and enterprises to take these technologies to market commercialization.7

Four Ways Washington Misunderstands What Should Government Do

Even if the Washington policy community were to agree that the United States faces a serious competitiveness challenge and needs a proactive federal policy, the key question is what kind of policy? Many fall short of supporting strategic industry policy because of flawed ideas of innovation and competitiveness.

Flawed Concept #6:

Capital Accumulation Is the Key

For many economists, the single most important driver of growth is “capital accumulation” (e.g., higher amounts of investment), and since investment requires savings, the single most important thing government can do to spur growth is to enact policies that boost national savings. For conservatives, this means boosting private savings through tax cuts on top marginal rates and capital (capital gains and dividends). For moderates, it means boosting public and private savings, reducing budget deficits, and helping low-income people save more.8 However, it is not the amount of capital that drives growth, but the demand for capital–and that demand comes from innovation. As U.C. Berkeley economist Brad Delong has explained, “Growth accounting studies in the tradition of Solow have found that capital deepening is responsible for only a small part of advances in labor productivity.”9 Moreover, in an environment where there is a surplus of capital and record-low interest rates, it is increasingly difficult to keep up the fiction that the supply of capital is the key driver of investment.

Flawed Concept #7:

Start-Ups and New Technologies Are Enough

Many believe that American can succeed if it only supports entrepreneurial activities, and that extending the lives of existing firms and technologies is not required. That is, it’s all about “new,” not “renew.” As such, the favored policies focus on speeding this introduction of front-end innovation through programs and policies to spur firm start-up and commercialization of new technology breakthroughs, as well as tough antitrust enforcement.

The reality is no matter how many new firms are started, if we don’t slow down firm death and contraction we will find ourselves like Alice in Wonderland, where it takes “all the running you can do, to keep in the same place,” creating new firms, only to see other nations, especially China take over the market.

Flawed Concept #8:

All We Need Is Better Innovation Inputs

Among those who recognize the need for government to act, many believe this role should be limited to supporting factor conditions (e.g., free trade, a good regulatory system, and intellectual property protection) and inputs that all firms can benefit from (e.g., basic research, an educated workforce, and infrastructure). For them, the problem is not within enterprises, it’s that enterprises lack the necessary inputs for successful innovation. Emblematic was a 2006 report from the Council on Competitiveness, which argues “Education is perhaps the single biggest threat to future American prosperity.”10

But while government surely needs to do more to support “factor conditions,” this is woefully inadequate. As a 2010 report from the McKinsey Global Institute explains, “Global competitiveness of industry sectors in countries such as Japan, Korea, and Finland vary immensely, despite the fact they all exist under the same macroeconomic policy rubric … sectoral policy factors largely explain these differences in outcomes.”11

Flawed Concept #9:

We Can Win Without Helping Big Corporations, Especially Multinationals

Finally, even when some recognize there is a problem and see government as having a key role, it has become increasingly popular among progressives to reflexively oppose policies that help large multinational corporations.

The idea that America can be competitive with strong companies producing cars, jet aircraft, computers, software, Internet applications, and pharmaceuticals—and that policies can ignore helping these firms be more competitive–is completely unrealistic.

Conclusion

Getting to a new “Washington consensus” that supports the need for a robust strategic industry policy will require more policy makers, experts and pundits changing their ideas. As Keynes once said, “when the facts change, I change my mind.” We need more people like Keynes.

This means jettisoning out-of-date, anachronistic ideas and proceeding along a series of logical steps laid out here. If one accepts the validity of the claims at each of these steps, then the only logical conclusion is that maximizing U.S. economic welfare requires a national advanced-industry strategy. Most of America’s economic competitors “intervene” in their economies to help their traded-sector enterprises be more competitive. It’s time for the United States to do the same.

About the Author

Robert D. Atkinson is founder and president of the Information Technology and Innovation Foundation (ITIF), the world’s leading think tank for science and technology policy. He is an internationally recognized scholar, a widely published author, and a trusted adviser to policymakers, with expertise in the broad economics of innovation.

Robert D. Atkinson is founder and president of the Information Technology and Innovation Foundation (ITIF), the world’s leading think tank for science and technology policy. He is an internationally recognized scholar, a widely published author, and a trusted adviser to policymakers, with expertise in the broad economics of innovation.

Twitter: @robatkinsonitif

References

1. Joseph S. Nye, “Declinist Pundits,” Foreign Policy, October 8, 2012, https://foreignpolicy.com/2012/10/08/declinist-pundits/.

2. Lawrence H. Summers, “No trade deal can dictate our relationship with China,” The Washington Post, February 4, 2019, https://www.washingtonpost.com/opinions/no-trade-deal-can-dictate-our-relationship-with-china/2019/02/04/ff5ea754-28c4-11e9-8eef-0d74f4bf0295_story.html.

3. Council on Competitiveness, Competitiveness Index, 30.

4. The Causes of the Trade Deficit, Before the U.S. Trade Deficit Review Commission (1999) (statement of Robert A. Blecker, Professor of Economics, American University).

5. Paul Krugman, “Competitiveness: A Dangerous Obsession,” Foreign Affairs 73, no. 2 (1994): 28–44.

6. Phil Gramm and Mike Solon, “Peace Through Strength Requires Economic Freedom,” The Wall Street Journal, March 1, 2022, https://www.wsj.com/articles/peace-through-strength-economic-freedom-open-trade-china-ccp-economy-america-competes-act-antitrust-biden-11646154226?page=1.

7. Michael Lind, Land of Promise: An Economic History of the United States (New York: HarperCollins, 2012).

8. Gene Sperling, The Pro-Growth Progressive: An Economic Strategy for Shared Prosperity (New York: Simon & Schuster, 2005).

9. J. Bradford DeLong, “Productivity Growth and Investment in Equipment: A Very Long Run Look” (working paper, Harvard University, 1991), 4.

10. Richard McCormack, “Council on Competitiveness Says U.S. Has Little to Fear, but Fear Itself; By Most Measures, U.S. Is Way Ahead of Global Competitors,” Manufacturing and Technology News, November 30, 2006, http://www.manufacturingnews.com/news/06/1130/art1.html.

11. James Manyika et al., How to Compete and Grow: A Sector Guide to Policy (New York: McKinsey Global Institute, 2010), http://www.mckinsey.com/mgi/publications/competitiveness/index.asp.

{kind=link}